- The DTC Times

- Posts

- Dream Big, Sell Smart: Navigating Exits in DTC

Dream Big, Sell Smart: Navigating Exits in DTC

Also more martech bugs and Google failings

Exits.

(Almost) every fouder dreams of them.

Not just any exit, either. BIG exits.

3X Revenue! 10x EBITDA!

It’s fun to dream, but what’s actually realistic when it comes to consumer brands and e-commerce companies?

Because we’re not in the realm of pre-revenue tech unicorns selling for billions, it helps to know what to shoot for if you really want an exit in your future.

This week:

How to achieve an exit as a subscale brand

More marketing tech bugs

We’ve lost Google to the dark side

Quick hits ← Find a Chrome extension for grabbing Facebook ad Id’s here.

So, you wanna sell?

For most, it’s not going to be about how many times your EBITDA you’ll get - it’s whether you can sell at all.

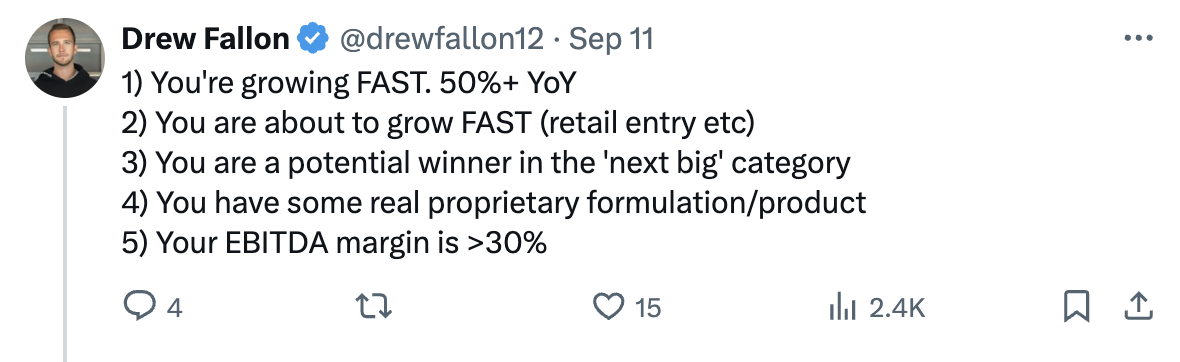

Drew Fallon, CEO of Iris Finance, says he often gets asked: “Hey Drew - my company does $2M of EBITDA a year. What is it worth if I sold it? We're in X category.”

Here’s the thing, if your EBITDA is $2 million or less, you’re probably sub-scale. And that’s an issue.

Why scale matters

A buyer of your brand is naturally looking to get a return on their investment. Anything sub-scale (less than $5M EBITDA) means a long repayment period at any kind of worthwhile multiple.

If you’re a smaller consumer company, it also means you haven’t grown big enough to establish yourself as “known” in your niche (brand equity). And you probably haven’t achieved operating economies of scale either.

Keep in mind, that your EBITDA ratio also matters. A purchaser will likely want to see something at around 10% to even be interested.

Unfortunately, it can be challenging for smaller-scale companies to consistently hit or beat a 10% threshold, often because they don’t have the economies of scale (as mentioned) or they are forced to reinvest cash back into the business to grow it.

The exceptions

All of the above is generally true, but you don’t always have to approach 9 figures to get a worthwhile offer.

One example from tech - the 40% rule.

The heuristic is: If your revenue growth rate + your EBITDA = 40%, you are likely considered a good purchase candidate.

As far as we know this isn’t explicitly applied in consumer (yet), but the principle of considering high growth vs high net cash is sound.

Also, on rare occasions, there are advantages to being small.

In this talk, the late Charlie Munger explains how a business travel magazine they owned got beat out by a smaller publication that specifically targeted corporate travel departments. In Charlie’s words: “Occasionally, scaling down and intensifying gives you a big advantage”.

In the same manner, Drew lists a few exceptions where potential investors might give you a worthwhile offer even if you technically a “subscale” brand:

Awesome growth rates are self-explanatory.

You being in the “next big” category means it’s ok if you haven’t achieved scale yet, you’re going to.

Having some IP means you can own and defend a piece of the market.

Your EBITDA margin being above 30% means you’re printing money.

Takeaway: If you haven’t unlocked serious scale, it might not be time to try and sell your company. There will either be little interest or the resulting multiple valuation will be steeply discounted.

If you’re not going to hit $50M+ any time soon but you still want an exit, you’ll need to tick some (most?) of the boxes Drew lists above.

Tool of the Week

If your brand is on the journey to 8, 9 or 10 figures, one thing is for certain - you will face a cash crunch at some point.

Even if your meta ads are crushing. Even if your inventory management is on point.

There usually comes a time when cashflow just doesn’t line up properly.

Every new region and sales channel requires more time, attention, and dollars.

The problem is big banks move slow and ask for guarantees.

You can go the equity route, but no one wants to give away ownership to what they built.

This is where Clearco steps in.

They fund invoices and receipts for everything from inventory to marketing, shipping, and logistics.

They simply just tick all of the boxes.

No collateral

Non-dilutive

Capped weekly payments

No personal guarantees

Best of all, they can turn things around QUICK. Like - get you funded in as little as 24 hours kind of quick.

So, if you’re looking for some financial support to gear up for Q4 and take your brand to the next level, check out Clearco and find out what they can do for you to get your ecommerce business funded.

BUGS ALERT

This week, a plethora of major marketing platform bugs to be aware of.

A bug cocktail, if you will.

Klaviyo - Apple bounces

A bunch of his brands have seen 100% email bounce rates when sending to Apple users.

Apparently, it has nothing to do with the usual deliverability issues (i.e. domain reputation etc).

Klaviyo is aware and working on a solution. Noah recommends excluding Apple users from campaigns for a few days.

More Meta changes - custom audiences

We’re being nice and listing this as a “bug”.

According to an email sent out to advertisers, Meta “plans to automatically restrict certain data, including parts of URLs and custom parameters.”

Furthermore, “custom audiences and ad sets may be affected or paused.”

Oh, and we don’t know when the changes come into effect. Yay.

Cory Dobbin from Shoelace says he’s seeing performance on Lookalikes drop this week, which he thinks might be early signs of the rollout.

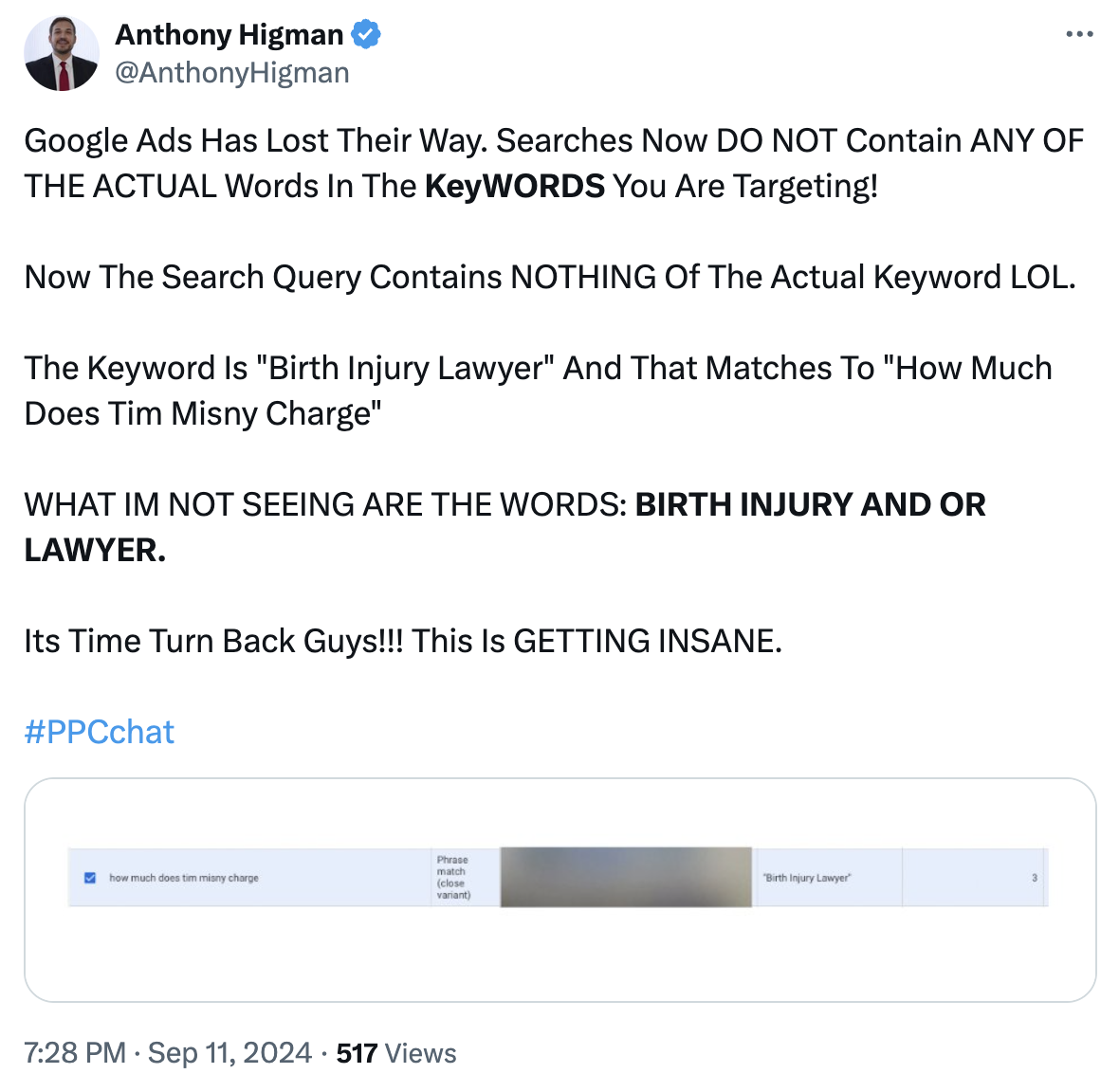

Google - doesn’t care about your keywords

Also not really a bug.

Takeaway: As if DTC isn’t hard enough already, right?

Google failing their “don’t be evil” mission

The anti-trust trial is underway against Google, and on day 3, some shady things were uncovered.

Hat tip to Jason Kint from Digitalcontentnext.org for the coverage on X.

Google imposed debt on Publishers

The DOJ expert, Dr. Ravi, explains that Google’s practices, particularly with Dynamic Revenue Sharing (DRS), allowed Google to delay payments to publishers while benefiting from the money in the interim.

This is referred to as "imposing debt" because it ties up the funds publishers should have received, while Google retains control over the timing of payments.

Google's Auction Manipulation (First Look and Last Look)

First Look: Google’s AdX ad exchange reportedly gave Google preferential treatment in auctions by letting it "jump the line" and win 53% of auctions due to its early access to bidding information.

Last Look: Google is accused of having the ability to view the top bid in auctions (essentially opening a "silent auction envelope") and then outbid that offer when necessary, further distorting the ad market.

Bid Manipulation

Bid Shaving: Dr. Ravi also explains that Google manipulated bids in its favor using practices like bid shaving, where Google could lower its bid or raise it when competitors (like AppNexus) were about to win high or low-value impressions. Competitors couldn’t do the same to Google.

Takeaway: There’s more and more evidence that Google has found ways to bend the rules of its own adtech to give itself an advantage.

Now we know why they removed their “don’t be evil” motto from their code of conduct a few years ago.

Quick hits

Chris Rudy from Adacted.com has built a browser extension to help you grab Facebook Post IDs. What a G.

Chad Carleton beautifully recounts the downfall of Blendtec to Vitamix with some valuable brand lessons on the way.

Quick tip from Marin Istvanic: keep a daily log and daily report of your ad account so you can track changes and impacts clearly.

Looking to pitch a big box retailer? Here’s what they are looking for before they put you on their shelves.

Reply